JobSeeker Income Test Explained (2026): How Earnings Affect Payments

The JobSeeker Payment is the primary income support safety net for Australians aged between 22 and Age Pension age who are looking for work, or who are temporarily unable to work due to illness. While its primary purpose is to support the unemployed, Centrelink actively encourages recipients to take on casual, part-time, or short-term contract work to maintain their connection to the workforce.

However, the moment you secure a few shifts and start earning wages, a complex set of mathematics comes into play: the JobSeeker Income Test.

The government does not simply cut off your JobSeeker payment the minute you earn a single dollar. Instead, they use a tiered system designed to slowly reduce your welfare payment as your private income increases. This ensures that you are always financially better off working than you would be relying solely on Centrelink. Yet, failing to understand how this test works—particularly the rules around “gross” income reporting and the dreaded taper rates—frequently leads to severe financial anxiety, payment suspensions, and crushing Centrelink debts.

In this comprehensive 2026 guide, we will have the JobSeeker Income Test explained in plain English. We will break down exactly how much you can earn before your payments are touched (the Income Free Area), how the Working Credit system can protect your payments during short bursts of employment, how your partner’s income impacts your claim, and the exact step-by-step process for reporting your wages securely via myGov.

Key Takeaways

- Gross vs Net: You must always report your gross income (the amount your employer pays you before tax is deducted). Reporting net income is the number one cause of Centrelink debts.

- The Income Free Area: You are allowed to earn a base amount each fortnight (historically around $150) without it affecting your JobSeeker payment at all.

- The Taper Rate: Once you earn above the free area, your JobSeeker payment is reduced by 50 cents, and eventually 60 cents, for every extra dollar you earn.

- Working Credits: If you don’t work for a while, you build up Working Credits. These act as a shield, allowing you to earn more than the free area without your payment reducing, making it highly beneficial to take short-term casual jobs.

- Partner Income: If you live with a partner, their income is also tested. If your partner earns a high salary, your JobSeeker payment may be reduced to zero, even if you are entirely unemployed.

What is the JobSeeker Income Test?

To ensure welfare is directed only to those who genuinely need it, Services Australia applies two tests to every JobSeeker applicant: the Assets Test and the Income Test.

The Assets Test looks at the total value of what you own (savings, cars, investment properties). The Income Test looks at the money you have coming in right now. Centrelink assesses your income every 14 days (your fortnightly reporting period).

Income is not just wages from a job. Under the Income Test, Centrelink also counts:

- Casual, part-time, or full-time wages.

- Business income if you are a sole trader.

- Rental income from investment properties.

- Deemed income from financial investments (shares, large bank balances).

- Paid parental leave or worker’s compensation.

If the total amount of income you receive in a 14-day period exceeds specific thresholds, your JobSeeker payment for that specific fortnight will be reduced.

How It Works: Free Areas and Taper Rates

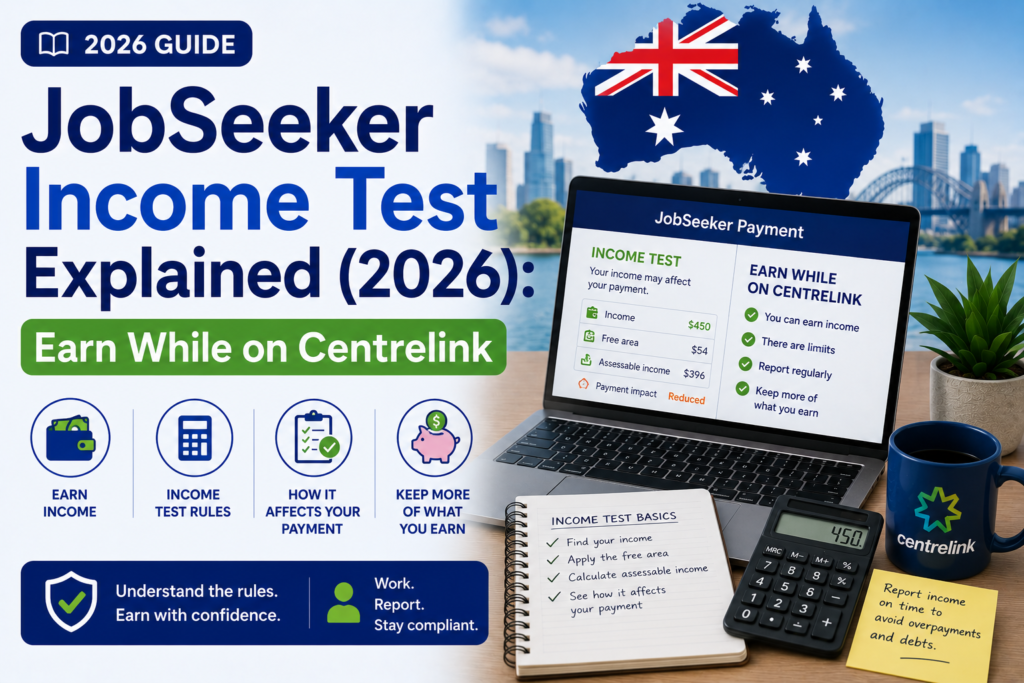

To calculate exactly how your wages will impact your payment, you need to understand two concepts: the Income Free Area and the Taper Rate. (To skip the manual math, use our Benefits Calculator to estimate your payment).

The Income Free Area

The government wants you to work. To incentivize this, they give you an “Income Free Area.” This is the amount of gross money you are allowed to earn in a fortnight before your JobSeeker payment is touched.

While the exact figure is indexed and changes periodically, a standard single person with no children can typically earn around $150 per fortnight before their payment is affected. If you work a 4-hour shift at a cafe and earn $120 gross, your JobSeeker payment remains at its maximum rate. You keep your wages AND your full Centrelink payment.

The Taper Rate (50c and 60c Reductions)

Once your earnings exceed the Income Free Area, the “Taper Rate” kicks in. This is the rate at which Centrelink claws back your welfare payment.

The JobSeeker taper rate is historically tiered:

- The 50-cent tier: For income earned between the free area (e.g., $150) and a secondary threshold (e.g., $256), your JobSeeker payment is reduced by 50 cents for every dollar you earn.

- The 60-cent tier: For any income earned above that secondary threshold (e.g., over $256), your JobSeeker payment is reduced by 60 cents for every dollar you earn.

The math in action: If you earn an extra $100 in the 60-cent tier, your employer pays you $100, but Centrelink reduces your JobSeeker by $60. You are still $40 better off than if you hadn’t worked at all, but the financial benefit of working diminishes the more you earn, until your JobSeeker payment eventually hits $0.

Working Credits: Your Secret Weapon

The harsh reality of the taper rate often discourages people from taking short-term, intensive jobs (like working at a festival for a weekend or doing 3 days of heavy labor). To counter this, Centrelink uses the Working Credit system.

If your total income is below the Income Free Area in a fortnight (for example, if you are completely unemployed and earning $0), you accrue Working Credits. You can build up a maximum balance of 1,000 Working Credits.

When you eventually get a job and your income exceeds the Income Free Area, Centrelink will automatically deplete your Working Credits before they apply the taper rate to reduce your JobSeeker Payment. One Working Credit equals one dollar.

Example: You have 500 Working Credits saved up. You get a temp job and earn $400 over the limit this fortnight. Normally, your JobSeeker would be slashed. However, Centrelink deducts 400 credits from your balance instead. Your JobSeeker payment remains at the absolute maximum, meaning you get a massive financial boost for that fortnight.

The Partner Income Test

If you are married or living in a de facto relationship, Centrelink treats you as a couple. This means you are subject to the Partner Income Test.

Even if you are 100% unemployed and aggressively looking for work, if your partner has a high-paying job, their income will reduce your JobSeeker payment. Your partner is granted a separate Partner Income Free Area (which is substantially higher than the single free area). Once your partner’s income exceeds this threshold, your JobSeeker payment will begin to taper off (usually by 60 cents for every extra dollar your partner earns).

Many individuals find that they are completely ineligible for JobSeeker because their spouse earns a solid full-time wage, regardless of the applicant’s own lack of income. If you are struggling to navigate partnered claims, refer to our Application Support Guide.

Step-by-Step Process: How to Report Income

When you are on JobSeeker, you must report your income (and confirm you have met your mutual obligation job searches) every 14 days on a specific reporting date. If you fail to report, you do not get paid.

- Know Your Dates: Your 14-day reporting period has a specific start and end date. You must only report income earned within those exact dates.

- Use the Digital Tools: The fastest way to report is via the Express Plus Centrelink App on your smartphone, or by logging into your myGov account on a computer.

- Calculate Gross Pay: Look at your payslips. You MUST enter the Gross Amount (the big number before tax, HECS, or superannuation deductions).

- Enter Hours Worked: You must also accurately report the total number of hours you worked during the 14 days.

- Declare Partner Income: If applicable, you must also report the gross amount your partner earned during the exact same 14-day window.

- Submit: Once submitted, the app will instantly calculate your taper rate and tell you exactly how much your upcoming JobSeeker payment will be.

Crucial Rule Change: In the past, you reported income when you earned it. Now, you must report income when it is paid to you. If you work in week 1, but your boss doesn’t pay you until week 3, you report that income in the reporting period covering week 3.

What Happens if You Earn Too Much? (Zero Rate)

If you take on a full-time job, your earnings will easily exceed the upper threshold, and the taper rate will reduce your JobSeeker payment to $0.

This is a positive outcome, but it doesn’t mean your Centrelink relationship ends immediately. Centrelink will place you in a “Zero Rate” period. You can have up to six consecutive fortnights where your payment is $0 due to employment income without your JobSeeker claim being cancelled.

During this Zero Rate period:

- You must continue to report your high income every 14 days.

- You get to keep your Health Care Card or Pensioner Concession Card, granting you access to cheap medicine.

- If you lose your new job or your hours are slashed within those 12 weeks, your JobSeeker payments will automatically restart without you having to submit a brand new, lengthy application.

If you earn enough to receive $0 for more than 6 consecutive fortnights (12 weeks), Centrelink assumes your employment is stable, and they will officially cancel your JobSeeker claim.

Common Mistakes and Centrelink Debts

The JobSeeker Income Test is unforgiving of administrative errors. Avoid these common traps:

- Reporting Net Income: We cannot stress this enough. If you report the money that lands in your bank account (net pay), you are under-reporting your income. Centrelink cross-references your reports with Single Touch Payroll data from the Australian Taxation Office (ATO). They will catch the discrepancy, and you will be issued a debt for overpayment.

- Reporting on the Wrong Dates: If your boss pays you on a Friday, but your reporting period ended on Thursday, you must wait until your next reporting fortnight to declare that money. Do not declare it early.

- Ignoring Small Jobs: Doing cash-in-hand work (like mowing lawns or babysitting) and not reporting it is welfare fraud. All income must be declared, even if it is below the free area.

Frequently Asked Questions

Does Rent Assistance reduce if I work?

Yes. If you receive Rent Assistance as part of your JobSeeker package, the income test applies to your total payment. Once the taper rate reduces your base JobSeeker to zero, any further income will begin to reduce your Rent Assistance until it is also zero.

Do I report my income before or after tax?

You must always report your income BEFORE tax. This is known as your Gross Income. It is usually the largest number on your payslip.

What happens if I forget to report on my reporting day?

If you fail to report your income and job searches on your assigned reporting date, your JobSeeker payment will be suspended. You will not get paid. You can usually log in the next day to complete the report late, but your payment will be delayed accordingly.

Are my Working Credits reset every year?

No, Working Credits do not expire at the end of the financial year. They remain in your account until you use them (up to a maximum balance of 1,000 credits) or until your JobSeeker claim is cancelled.

Official Resources

For the exact, current dollar figures regarding Income Free Areas and Taper Rates (which change with inflation), always check the official government pages:

Conclusion

Navigating the JobSeeker Income Test can feel like walking a financial tightrope, but it is fundamentally designed to ensure that you are always financially better off by participating in the workforce. Taking on a few shifts a week will boost your overall household income, provide valuable experience for your resume, and fulfill your mutual obligation requirements.

The secret to avoiding the anxiety of Centrelink compliance lies in aggressive organization. You must understand your 14-day reporting cycles, track your Working Credits, and most importantly, habitually report your gross income via your myGov account exactly on time.

If your hard work leads to full-time employment and your payments taper down to zero, embrace the 12-week safety net period. It provides peace of mind knowing that if the new job doesn’t work out, your JobSeeker support is ready to seamlessly restart.

Disclaimer

PublicServicesDesk.com is an independent informational website and is not affiliated with, endorsed by, or operated by the Australian Government, Services Australia, Centrelink, Medicare, MyGov, the Australian Taxation Office (ATO), or the Department of Home Affairs. Information is provided for general educational purposes only and may change over time. Always verify important details through official Australian Government websites before making decisions or submitting applications.